Thinking of retiring soon and would want to save more but avoid the future tax penalty as a high earner? You may have hit your 401(k) limit and you think to yourself, so what? The answer is the Mega Backdoor Roth. It is a sophisticated, IRS legal strategy that has the capacity to turbo-charge your tax free retirement savings.

We will simplify it in the easiest manner in this guide. You will know how this plan functions, how much you can donate, and what regulations of the IRS are involved. At the end, you will understand why this move is preferable among high earners in income who are seeking their retirement growth to be tax free and they take it very seriously.

Table of Contents

What is the Mega Backdoor Roth?

The Mega Backdoor Roth allows high earners to contribute far beyond the standard Roth IRA limits by leveraging after-tax 401(k) contributions, then rolling them into a Roth IRA or Roth 401(k). If your employer plan supports it, you could potentially contribute over $40,000 more per year to Roth accounts.

Why It Matters

- Standard Roth IRA contribution limits for 2025 are only $7,000 ($8,000 for those 50+).

- High earners are often ineligible to contribute directly to a Roth IRA due to income phaseouts.

- This strategy bypasses income limits and supercharges your Roth savings potential.

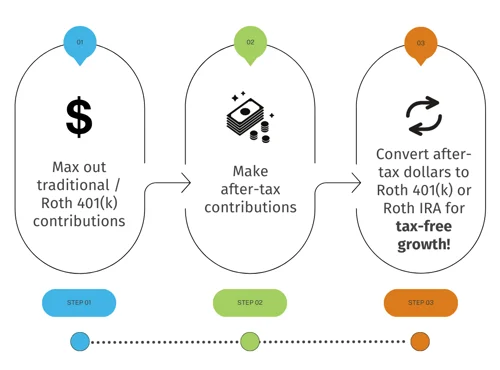

The Mega Backdoor Roth Explained

Step 1: Use After-Tax 401(k) Contributes

- Exceed your customary boost pre-tax or Roth 401(k).

- As of 2025, the combined limit on 401 (k) contributions (employee + employer + after tax) is 69, 000 (76, 500 at age 50 and above).

- E.g. you contribute 23,000 and your employer contributes 5,000, you can put an additional 41,000 after-tax.

Step 2: Your Plan Should permit In Service Withdrawals or Automatic Conversions

- The rules of in-service distribution (making withdrawals of after-tax contributions during employment) must be allowed by your plan.

- There are schemes that auto-convert such post-tax funds to Roth 401(k).

Step 3: convert to Roth IRA or Roth 401(k)

- You transfer to a Roth IRA the post-tax retirement savings to the 401K.

- When done right, you do not pay taxes, or have to pay minimal ones, since the money is already taxed.

Step 4: Grow tax-free and make tax free withdrawals

- When put into Roth, the money increases without tax.

- Withdrawals in retirement are also tax-free provided that it is a qualified one.

Mega Backdoor Roth vs Backdoor Roth IRA

| Strategy | Who is it for? | Contribution Potential | Complexity |

| Backdoor Roth IRA | High earners without Roth IRA access | $7,000/year | Simple: non-deductible IRA to Roth |

| Mega Backdoor Roth | High earners with 401(k) access | $40,000+ (varies) | Advanced: after-tax 401(k) to Roth |

The Mega Backdoor Roth allows significantly larger Roth contributions.

IRS Rules You Must Follow

- 401(k) plans must allow: after-tax contributions and in-service rollovers.

- Earnings on after-tax funds are taxable upon conversion.

- Must follow IRS pro-rata rule Roth IRA guidelines to avoid unwanted taxes.

- 🔍 Key Benefits

- Maximize retirement savings well beyond traditional limits.

- Tax-free retirement growth without annual income phaseout concerns.

- Ideal for high-income Roth IRA strategies.

- Helps with tax diversification in retirement.

Common Pitfalls and How to Avoid Them

Not All 401(k) Plans Allow It

Check your 401(k) plan customization with HR to confirm eligibility for after-tax contributions and in-service withdrawals.

Pro-Rata Rule Trouble

To avoid the pro-rata rule, convert only the after-tax portion—not pre-tax earnings.

Timing Issues

Convert or roll over quickly to avoid accumulating taxable earnings. Use the IRS rules for Roth IRA timing carefully.

Tax Diversification: Why It’s Important

Tax diversification means having a mix of taxable, tax-deferred, and tax-free accounts. The Mega Backdoor Roth fills the tax-free bucket:

- Protects against future tax hikes.

- Offers withdrawal flexibility in retirement.

- Minimizes required minimum distributions (RMDs).

Advanced Roth Planning to High Income Earners

- It is suitable where one is unable to contribute the maximum levels in their regular retirement program but wants to do a high earner retirement program.

- Organize with the other tools such as the non-deductible IRA contributions or the traditional vs Roth IRA choices.

- Major long-term savings may be generated through strategic 401(k) to Roth IRA rollovers.

Mega Backdoor Roth at Work: An Example

Assume:

- Prior to tax, you invest in 401(k) by contributing 23000 US$

- Employer provides a match of 5000 dollars

- IRS overall cap = 69 000

- You make a total of after-tax contributions of 41,000 dollars.

- You put your $41,000 into a Roth IRA

- More than 20 years with 7 per cent = 158, 000+ tax free

Mega Backdoor Roth FAQ

Is the Mega Backdoor Roth legal? Yes, but only if your employer’s plan allows after-tax contributions and in-service withdrawals or conversions.

Can I do it every year? Yes, as long as your plan supports it and you stay within the IRS limits.

What if I don’t convert right away? You’ll owe taxes on any investment earnings that accumulate pre-conversion.

Mega Backdoor Roth vs Other Strategies

| Strategy | Annual Max (2025) | Tax Benefit | Complexity |

| Roth IRA (direct) | $7,000 | Tax-free growth | Simple |

| Backdoor Roth IRA | $7,000 | Tax-free growth | Moderate |

| Mega Backdoor Roth | $40,000–$60,000+ | Tax-free growth | Advanced |

Conclusion:

Mega Backdoor Roth is one of the most brilliant and effective solutions for high-income earners who want to create a huge tax-free retirement account. Through a proper 401(k) plan and smart strategy, you are allowed to shift tens of thousands of dollars in post-tax money to Roth IRA annually. This offers you diversification of tax, additional flexibility, and the possibility to build your retirement accounts quicker and safer. Weigh your options and consider asking a qualified financial or tax advisor to help you come up with your own plan to make the most out of this very powerful retirement tool.

Meta Description:

In the following guidance, we will see how the mega backdoor Roth works, IRS regulations, and post-tax 401(k) strategies, and why it is the best tool to grow tax-free in retirement in 2025.